Quick answer

In Canada in 2026, your credit score is built from a small list of formal "tradelines" that Equifax and TransUnion accept. Almost everything else that proves financial discipline (rent, utilities, savings, group contributions, remittances) is invisible to bureaus by default. This article is the complete, current list of what actually builds Canadian credit, what almost-counts, and what does not count yet but should.

What "credit-building activity" actually means in Canada

A credit-building activity is any financial behavior that ends up as data on your Equifax Canada or TransUnion Canada file. Without that data, your score does not move. The behavior can be virtuous on every other measure (you save half your income, you pay every bill on time, you support extended family), but if it does not reach a bureau, it does not change your score.

There are three categories that matter:

- What counts today, automatically: accounts that report to one or both bureaus by default.

- What counts today, only if you opt in: services that report your behavior to bureaus only if you sign up or your provider participates.

- What does not count yet: real financial activity that bureaus do not currently accept, but that some are working to recognize.

If you read only one section, read category three. That is where most newcomers and thin-file Canadians live, and where the system is unfair.

Category 1: what counts today, automatically

These accounts report to Canadian credit bureaus the moment they exist. Open them, use them on time, and your score builds without you doing anything else.

| Activity | Reports to | Notes |

|---|---|---|

| Credit cards (secured and unsecured) | Equifax + TransUnion | Most powerful single activity |

| Auto loans | Equifax + TransUnion | Installment tradeline |

| Personal loans from chartered banks | Equifax + TransUnion | Installment tradeline |

| Mortgages | Equifax + TransUnion | Largest possible installment |

| Lines of credit (LOC, HELOC) | Equifax + TransUnion | Revolving tradeline |

| Student loans (federal and provincial) | Equifax + TransUnion | Installment tradeline |

| Some retail-store cards | Usually Equifax + TransUnion | Confirm with the issuer |

| Buy-Now-Pay-Later (BNPL) on larger purchases | Increasingly both bureaus | Affirm Canada, Klarna Canada report; smaller BNPL still inconsistent |

These are the bedrock. A Canadian credit file with three to four active tradelines in this list, paid on time for 24 months, will sit comfortably above 700.

Category 2: counts today, only if you opt in or your provider participates

These accounts can report to bureaus, but the link is not automatic. You usually have to enroll, ask, or pick a participating provider.

| Activity | What unlocks reporting |

|---|---|

| Rent payments | Participating property managers report through services like RentReporters, FrontLobby, or Borrowell Rent Advantage. Most landlords do not participate by default. |

| Utility payments (hydro, water, gas) | A handful of Canadian utilities have begun reporting through Equifax pilots. Most do not yet. Status is regional and changes year to year. |

| Cell phone contracts | Postpaid plans report to bureaus automatically. Prepaid plans do not. |

| Internet contracts | Some major Canadian ISPs report postpaid accounts. Confirm with your provider. |

| Insurance premiums | Generally do not report. Some niche programs exist but are not mainstream. |

| Subscription services | Do not report. Even years of perfect Netflix or Spotify payments do nothing for your score. |

Category 2 is the most active frontier in Canadian credit reporting right now. Expect more activity here through 2026 and 2027 as Equifax and TransUnion both expand alternative-data programs.

Does paying rent build credit in Canada?

Not on its own. Paying rent on time builds credit in Canada only if those payments are reported to a credit bureau, and by default they are not. Your landlord does not send your rent history to Equifax or TransUnion, so years of perfect payments can leave no mark on your file. To make rent count, you have to route it through a rent-reporting service.

A few things are worth knowing before you sign up for one:

- Only Equifax counts rent today. Equifax Canada is the bureau that factors rent payments into a file, through partners like the Landlord Credit Bureau and Borrowell. TransUnion Canada does not currently use rent data, which is one reason your two scores can differ.

- Two enrollment models. Some services (such as Borrowell Rent Advantage) let you self-report by connecting your bank account, so you do not need your landlord to participate. Others (such as FrontLobby) require your landlord to create an account and submit the payments each month.

- It is most powerful for a thin file. If rent is one of very few things on your report, adding it can be the difference between having a usable Equifax score and having none at all.

- It costs money. Most rent-reporting services charge a monthly fee, usually in the ten to twenty dollar range. For a thin file that one tradeline can be worth it; for an already-established file the benefit is smaller.

Wiremi does not currently report rent to Equifax Canada or TransUnion Canada. Direct bureau partnerships are in progress so that the activity on your Wiremi Passport, rent included, eventually contributes to your traditional Canadian score. Until that is live, treat a dedicated rent-reporting service as the route that counts today, and use your Wiremi Passport as the verifiable record you carry to anyone who accepts alternative credit data.

Category 3: what does not count yet, but should

This is where the system is unfair, and where Wiremi was built. Real financial discipline, documented for years inside immigrant and diaspora communities, is invisible to Canadian bureaus.

Activities that do not yet build Canadian credit:

- Savings group contributions: njangi, ajo, susu, chama, sou-sou, paluwagan, kameti, chit funds, tanda, hui, partner-hand. Centuries-old rotating savings traditions that demonstrate exactly the consistency bureaus claim to measure.

- Cross-border remittances: Years of sending money home on a fixed schedule is one of the strongest commitment signals a human can produce. No Canadian bureau accepts it as a tradeline.

- Individual savings discipline: Putting $200 aside every payday for 24 months is invisible to your score unless it sits inside a credit-reporting product.

- Foreign credit history: Your full CIBIL, eCIB, CRC, CIC, or other home-country bureau report. Nova Credit translates a small list (UK, India, Mexico, others) for US lenders only. No equivalent exists for Canada.

- Cash rent paid on time: If your landlord does not participate in a rent-reporting service, your perfect rent history does not exist on your file.

- Mobile money history: MTN MoMo, M-Pesa, Orange Money, GCash, Maya, JazzCash, Easypaisa. None of it counts.

- Family support transfers: Supporting siblings, parents, or extended family is community standard in many cultures and economically equivalent to a recurring obligation. It is not a tradeline.

- Cooperative society and microfinance contributions: Common across West Africa, East Africa, South Asia, and Latin America. Not visible to Canadian bureaus.

The system measures consistency over time. The activities above are consistency over time. The gap is data collection, not behavior.

What this means for newcomers and thin-file Canadians

If everything you do well sits in Category 3, the Canadian credit system reads you as a stranger no matter how disciplined you actually are. The path forward is not to abandon Category 3 behavior. The path is to:

- Open Category 1 products as early as possible. A secured credit card on day three of arrival is worth more than waiting six months for a perfect plan.

- Opt into every Category 2 program available to you. Ask your landlord about rent reporting. Pick postpaid over prepaid. Confirm your utility provider's reporting status.

- Document Category 3 behavior somewhere verifiable. Wiremi exists to record the savings group contributions, cross-border transfers, and recurring commitments that bureaus do not yet accept. If you run a njangi inside Wiremi for two years, the data is real, exportable, and ready for the day Canadian bureaus accept alternative credit signals.

The unfairness is real but the path is mechanical. Time on file is the variable you cannot shortcut. Start the formal record today, keep the cultural record running on Wiremi, and the day bureaus expand what they accept, you will already have built it.

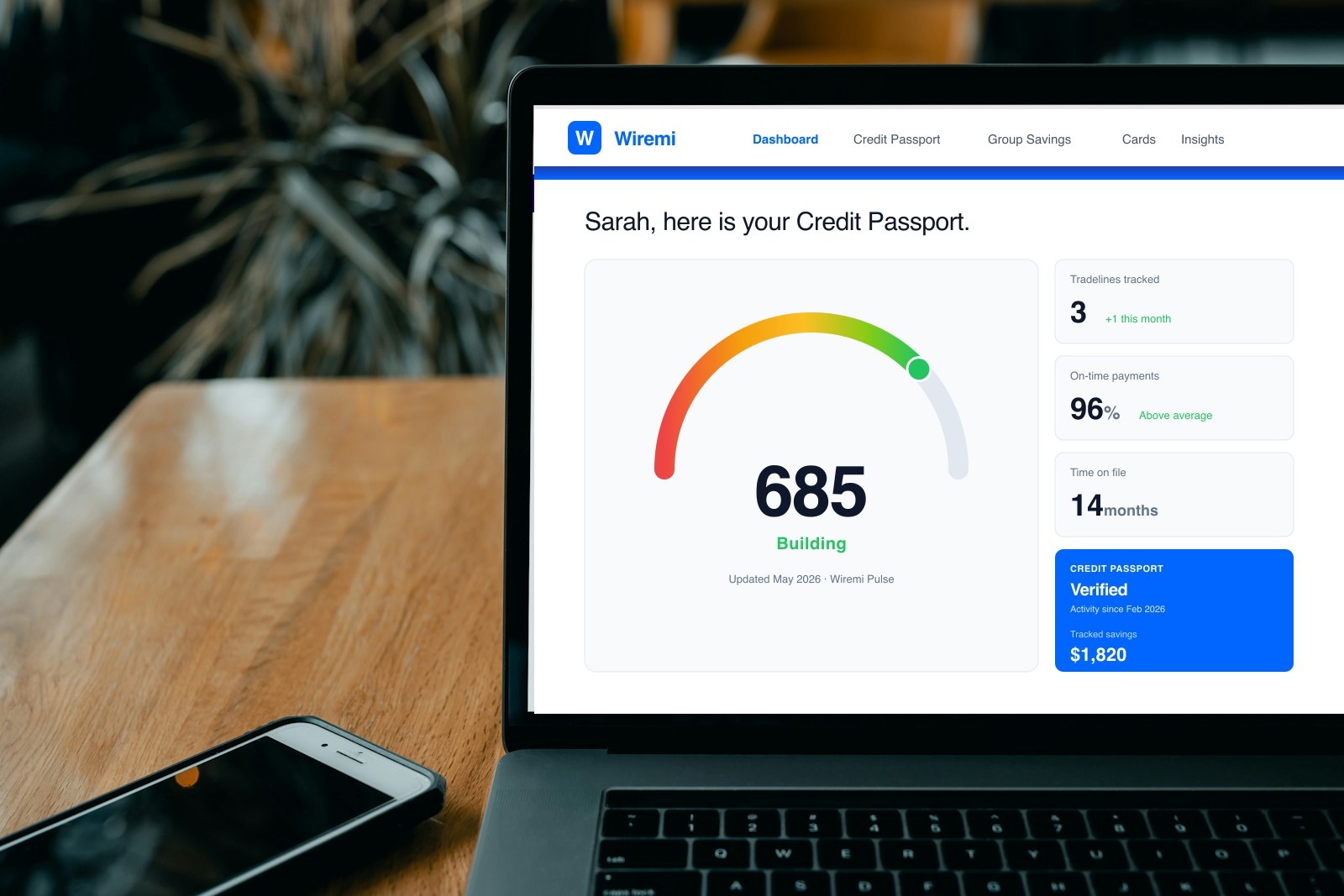

Where Wiremi fits

Wiremi was founded to close the Category 3 gap. The Wiremi Passport captures the financial behavior that should already count: savings groups, recurring transfers, savings goals, group-trust signals. Every contribution becomes verifiable evidence of consistency over time.

We are direct about what is not live yet. Wiremi does not currently report to Equifax Canada or TransUnion Canada. Direct partnerships with both bureaus are in progress so the activity on your Wiremi Passport eventually contributes to your traditional Canadian score. That part is not live. Until it is, your Wiremi Passport is the verifiable proof you carry to any lender, landlord, or institution that accepts alternative credit data, and the asset that will give you a head start when bureau partnerships activate.

The bottom line

Canadian credit in 2026 still rewards a narrow list of formal tradelines and ignores most of what actually proves financial discipline. The fastest score comes from opening Category 1 products early and opting into Category 2 wherever possible. The fair score comes from changing what Category 3 looks like, and that is the work Wiremi and a small set of others are doing. If you are reading this and you are doing Category 3 well, you are not behind. The system is.