Quick answer

A thin credit file means you have a credit history, but not enough of it. Canadian lenders generally want to see at least three active accounts and six months of activity before they offer their best rates. With less than that, your file reads as "thin," and you can pay more, or get denied, even with perfect payment behavior.

What is a thin credit file?

A thin credit file is the credit-bureau version of a half-empty resume. You have something on file, but lenders do not have enough information to confidently predict how you will handle a new loan, mortgage, or premium credit card.

Both Equifax Canada and TransUnion Canada will generate a credit score for you as long as there is at least one active tradeline. Scoring and approval, though, are two different things. A score can exist on a thin file. Approval at a fair rate usually cannot.

The phrase covers a few common situations:

- A new credit card opened in the last few months.

- One auto loan or one student loan, and nothing else.

- A line of credit that you pay off in full every month.

- A long history of paying cash for rent, phone, and utilities, with none of it reported to a bureau.

People often confuse a thin file with bad credit. They are different. Bad credit is a record of missed payments and collections. A thin file is the absence of enough record. One reads as "risky," the other reads as "unknown." Both get treated cautiously, but the fix is different.

How does it hurt you?

You can have a 740 score on a thin file and still hear "no." Or "yes, but at the worst rate." Here are the four places it shows up most often.

- Mortgage applications. Banks underwrite based on the score and file depth together. A thin file with a strong score often gets routed to B-tier or alternative lenders, where rates can run one to three points higher.

- Premium credit cards. Cards with travel insurance, cash back, and higher limits typically require at least two years of active credit history. Thin files get the basic version, not the premium one.

- Auto loans. Dealerships will approve thin-file applicants, but at sub-prime rates. The car costs the same. The financing costs much more.

- Apartment applications. Landlords in competitive Canadian markets routinely pull bureau reports. A thin file can lose you the unit to a stronger applicant, even when your rent budget is identical.

What counts as "thick enough"?

There is no single bureau-published threshold. Canadian lenders, though, generally treat a file as thick enough once it shows the pattern below.

| Factor | Thin file | Comfortably thick |

|---|---|---|

| Active tradelines | 1 to 2 | 3 or more |

| Age of oldest account | Under 12 months | Over 24 months |

| Mix of credit types | One product only | Revolving and installment |

| On-time payment history | Less than 6 months | Over 24 months |

| Recent hard inquiries | Two or more in 6 months | Spaced out, low volume |

The exact bar depends on the lender and the product. A credit card issuer is more forgiving than a mortgage underwriter. But the direction is consistent: more accounts, longer history, mixed types, clean payments.

How to fix a thin credit file in Canada

There is no quick fix, but there is a clear path. Start with the easiest moves and let time do the rest.

- Open a secured credit card if you do not have one. Pay a refundable deposit, use the card for small recurring purchases, and pay it off in full. The card reports to both bureaus and ages on your file every month.

- Add a second product after six months. If your first tradeline is a card, add a small installment loan or a credit-builder loan. Lenders score credit mix. A thin file with only one product type stays thin.

- Stop paying balances down to zero before the statement closes. Counterintuitive, but the bureau sometimes reads a zero balance as inactive use. Leave a small balance (5 to 10 percent of your limit), let the statement post, then pay it off in full.

- Get rent and utility payments reporting where you can. Some Canadian landlords participate in rent reporting services that send your on-time payments to Equifax. If yours does not, you can sometimes enroll yourself directly.

- Avoid new applications for at least six months before you need a major approval. Hard inquiries lower your score short-term and signal credit hunger to underwriters reviewing a thin file.

- Be patient. Time on file is the one factor you cannot speed up. Six months of clean reporting is the minimum lenders need to take you seriously. Twenty-four months is when your file starts to read as thick.

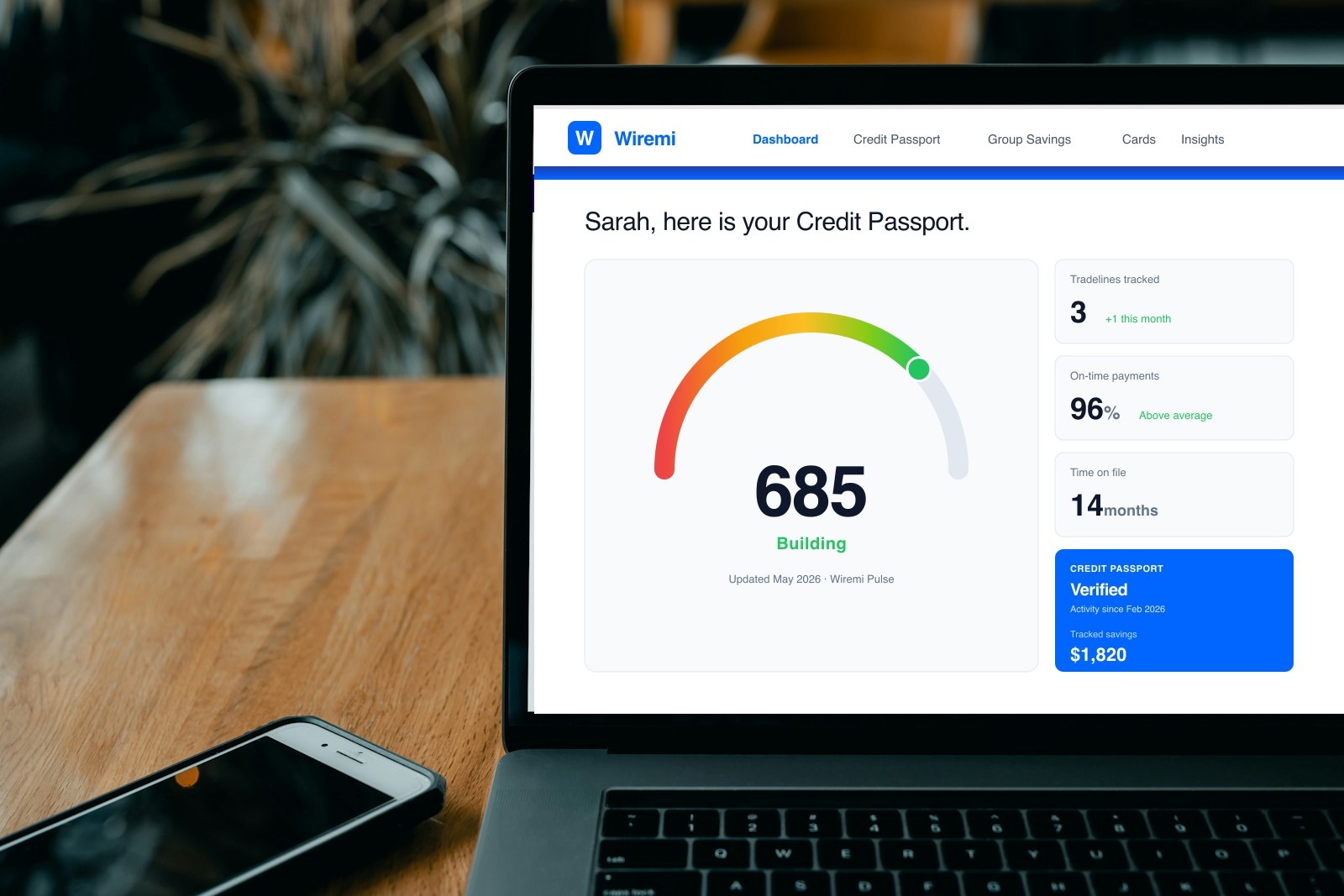

Where Wiremi fits

Wiremi tracks the activity that should already be on your credit file: rent payments, savings contributions, ROSCA participation (Njangi, Ajo, Susu, Chama, sou-sou, paluwagan), recurring bills, and consistent money behavior. We turn that into your Wiremi Passport, a verifiable record of how you actually handle money.

We are direct about what this is and is not today. The Wiremi Passport currently lives inside Wiremi. Lenders and landlords who accept alternative credit data can use it. We are working on direct partnerships with Canadian credit bureaus so this same activity counts toward your traditional Equifax or TransUnion file, rather than routing through third-party intermediaries. That part is not live yet.

In the meantime, the Passport is the proof you carry into conversations the bureaus do not cover. The traditional fixes above still apply: secured card, credit mix, time on file. Wiremi makes sure the rest of your financial behavior, the part the bureaus historically ignore, is not invisible.

The bottom line

A thin credit file is fixable. It usually takes the right two or three accounts, six to twenty-four months, and clean behavior. Most people overcomplicate it. The cost of doing nothing is real, higher rates, lost approvals, longer renting timelines, but the path out is mechanical, not magical. Pick the next move and start the clock.